By: Michael Hoover | 03/10/26

Key Takeaways

Restaurants often qualify for Research and Development Tax Credits through everyday innovation like menu development, new food items, kitchen process improvements, and operational technology

Qualified Research Expenses typically return about 6% to 12% in federal R&D tax credits that can be used in tax savings

There is a persistent belief that research and development applies only to software companies or pharmaceutical labs. In practice, the IRS definition is far broader. Any business that improves products, processes, or systems through experimentation may qualify.

Restaurants are constantly experimenting. A chef adjusting ingredient ratios to improve consistency, a team refining cooking times for scalability, or an operator implementing new ordering systems are all examples of technical problem solving. That is the core of what qualifies.

The key is not whether something is new to the world. It only needs to be new to your business and involve uncertainty. If your team did not know whether a new preparation method would achieve the desired quality, and you tested different approaches to get there, you are already within the framework.

The IRS evaluates this through a four-part test:

For a typical restaurant, these criteria are met far more often than expected. The industry’s push toward efficiency, cost control, and customer experience naturally drives qualifying activity.

Most qualifying work in restaurants looks like normal operations at first glance. The difference is whether there is experimentation and technical uncertainty involved.

Common qualifying activities include:

Activities that generally do not qualify include:

The distinction is subtle but important. If there is trial and error aimed at improving performance, the activity is likely eligible.

Once qualifying activities are identified, the next step is determining eligible costs. These are referred to as qualified research expenses.

There are three primary categories:

Additional considerations:

These R & D expenses form the foundation of the credit calculation. Proper documentation is critical, including time tracking, project descriptions, and cost allocation.

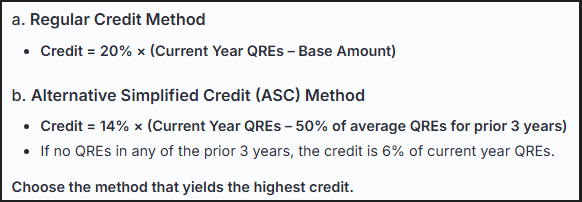

The calculation is based on qualified research expenses and can be approached through different methods, most commonly the regular credit method or the alternative simplified credit.

In the R & D tax credits food industry, qualified research expenses typically return about 6% to 12% in federal tax credits. These credits directly reduce tax liability on a dollar-for-dollar basis. That distinction matters. This is not a deduction. It is a credit against taxes owed.

For small or startup restaurants, there is an additional advantage. Under current rules:

Businesses can apply the credit against payroll taxes instead of income tax. This can provide up to $500,000 per year in immediate benefit, even if the business is not yet profitable.

This is where many early-stage operators miss an opportunity. They assume no income means no benefit. In reality, state payroll tax offsets can turn innovation into immediate cash flow.

Another often overlooked benefit is the ability to claim credits retroactively:

The result is a flexible planning tool that supports both current and future tax strategy.

The One Big Beautiful Bill Act introduced a major shift in how research costs are treated, and it directly affects restaurants investing in innovation.

Before 2022, businesses could immediately deduct research and experimentation costs. Then the rules changed, requiring those costs to be capitalized and amortized over five years. This created a mismatch between spending and tax benefit, tightening cash flow.

The new law reverses that issue for domestic activities:

For restaurants, this matters in practical terms:

There is also retroactive relief for smaller businesses:

In addition, all businesses can accelerate remaining unamortized costs:

This creates flexibility in timing and planning. A restaurant investing in process improvements or technology can now align tax benefits more closely with actual spending.

From a broader perspective, the law removes a barrier that had quietly discouraged innovation. It allows operators to pursue improvements in R&D performance without the drag of delayed tax relief.

Can a food startup with no income still benefit from the R&D credit?

Yes. In certain states, qualified small businesses can apply the credit against payroll taxes instead of income tax. If the business has less than $5 million in gross receipts and is within its first five years, it can claim up to $500,000 annually against employer payroll tax liabilities.

Does menu testing count as a qualified research expense?

It depends. Menu experimentation involving trial and error, ingredient changes, or process improvements may qualify. However, simple taste testing or cosmetic changes without technical uncertainty does not. The key is whether the activity involves a process of experimentation to improve performance or quality.

Can restaurants claim R&D credits for prior years?

Yes. Restaurants can typically claim credits for the current year and the three prior years by amending tax returns. Any unused credits may also be carried forward for up to 20 years, allowing businesses to benefit even if they cannot use the full amount immediately.

Is there a minimum amount of R&D spending required to claim the credit?

No formal minimum exists. However, the administrative effort should justify the benefit. Even modest levels of qualifying activity can produce meaningful credits, especially when combined over multiple years or applied against payroll taxes for smaller businesses.

How do state R&D credits interact with the federal credit for restaurants?

Many states offer their own Research & Development credits, which can be claimed alongside the federal credit. While rules vary, these credits generally provide additional savings and may follow similar definitions of qualified research. Coordinating federal and state claims can significantly increase total tax benefits.

Michael Hoover

Bennett Thrasher LLP

Phone: (770) 396-2200

Never miss an update. Sign up to receive our monthly newsletter to unlock our experts' insights.

Subscribe Now