A tech startup is evaluating a new project that promises high returns, but investors are cautious about the long-term risks. To address these concerns, the company conducts a discounted cash flow (DCF) analysis to determine whether the project’s potential benefits outweigh its associated risks.

This data-driven approach not only reassures stakeholders but also supports informed decision-making. In this article, we explore the principles of DCF analysis, its key assumptions, formula, and real-world applications.

Discounted Cash Flow (DCF) analysis is a valuation method used to estimate the value of an investment based on its expected future cash flows. By discounting these future cash flows to their present value, DCF analysis accounts for the time value of money, a principle stating that money today is worth more than the same amount in the future due to its earning potential.

DCF analysis is widely applied in finance, particularly in valuing stocks, businesses, projects, or any asset expected to generate cash inflows. The fundamental goal of DCF analysis is to determine whether an investment is worth more than its cost. If the calculated present value of future cash flows exceeds the investment’s current cost, it is deemed a profitable endeavor. Conversely, if the DCF is lower than the cost, it suggests the investment is not viable.

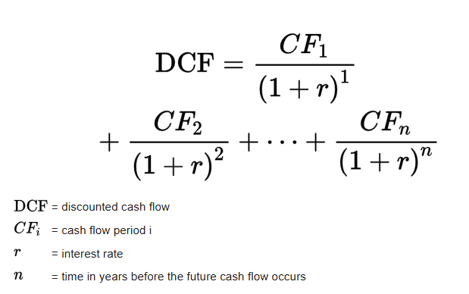

The formula for DCF is expressed as:

Each future cash flow is discounted back to the present using a discount rate, which often reflects the cost of capital. For businesses, this rate is typically the weighted average cost of capital (WACC), combining the costs of both equity and debt financing.

For example, consider a project requiring an initial investment of $150,000, expected to generate cash flows of $10,000, $10,000, $15,000, $25,000, and $20,000 over five years, with a terminal value of $100,000 in the fifth year. Using a 5% discount rate, the present value of these cash flows would amount to $146,142. Since this is lower than the initial investment, the project would not be recommended.

A successful DCF analysis relies on several critical assumptions:

The versatility of DCF analysis makes it a cornerstone of financial decision-making. Below are some of its primary applications:

DCF analysis remains a foundational tool in finance, enabling investors and companies to evaluate the viability of investments and projects. Despite its limitations, its ability to account for the time value of money makes it indispensable for long-term decision-making. By mastering how to run a discounted cash flow analysis, practitioners can develop reliable models for assessing potential returns and minimizing risks. Seeking professionals with expertise in DCF analysis can further enhance the accuracy and effectiveness of the evaluation, ensuring well-informed financial decisions.

For more than four decades, Bennett Thrasher has provided businesses and individuals with strategic business guidance and solutions through professional tax, audit, advisory, and business process outsourcing services. Contact Gina Miller, partner in charge of Bennett Thrasher’s Business Valuation Practice, or call us at 770.396.2200.

Never miss an update. Sign up to receive our monthly newsletter to unlock our experts' insights.

Subscribe Now